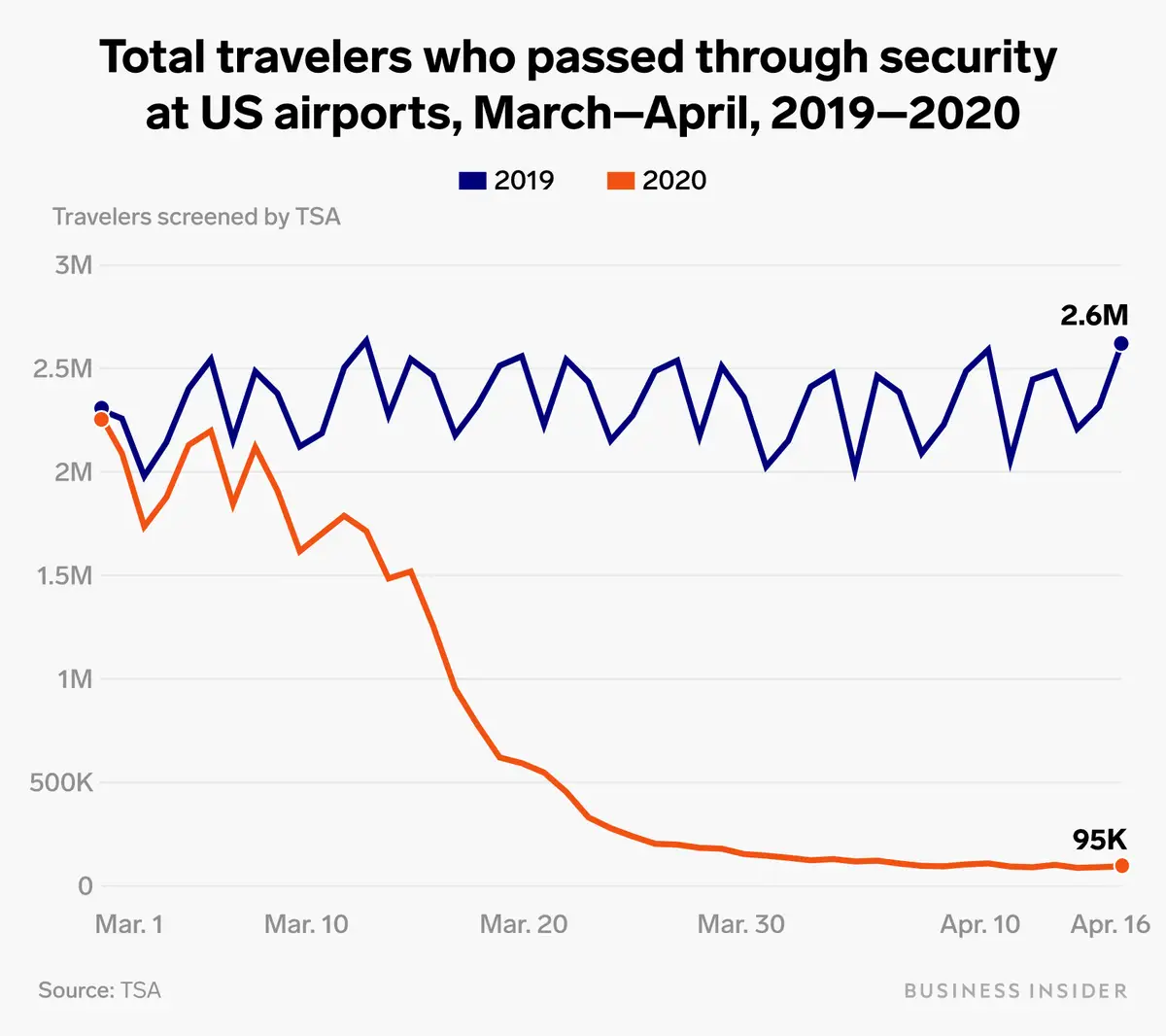

Spirit Airlines will survive the Coronavirus crisis. The company has $894 million in cash and has access to a revolving credit facility of $110 million which carries an interest rate of 2% plus the LIBOR and has the option to increase it to $350 million. Additionally, the company is slated to receive $330 million through the Payroll Protection Program. This means the company should have around $1.2 billion in liquidity with an option to increase it to $1.4 billion. The company’s primary expenses are from labor and fuel which combined account for ~50% of operating costs. The drop in oil prices and reduction in capacity will limit the $1 billion spent on fuel last fiscal year.

Spirit has also cut costs by delaying capital investment and other expenses by $70 – 105 million before any savings from a reduction in capacity. The company has stated that they reduced flight capacity by 80% in April and plan to reduce May capacity by 75%. These reductions should help save a large portion of the $3 billion spent last year on operating costs. Also, all tickets sold by the company are non-refundable, limiting the potential cost of refunding passengers. As long as Spirit can provide transportation, these pre-sold tickets will be recognized as revenue. Assuming a national shutdown does not last for an additional year, the company has adequate liquidity to survive the crisis. Additionally, Spirit is primarily a domestic carrier, meaning border shutdowns do not affect the company as adversely as it does the larger airlines.

Now that the question of survival has been settled, what are the company’s prospects? Currently, at a $13 share price, the company is trading at a price to ‘19 sales ratio of 1:5. Additionally, the company’s market cap is currently below the cash value on its balance sheet. However, the future of Spirit depends on factors largely outside the company’s control. The first question is: When will people fly like normal? The absolute latest time is when a vaccine or effective treatment becomes widely available. The earliest time would be when the U.S. government reduces restrictions and allows carriers to operate normally again and people act indifferent to the pandemic. The timeline on a return to normalcy is probably in the range of 3 – 14 months. With the innate flexibility of Spirit’s corporate structure, the company should be able to significantly cut costs and conserve cash.

However, will air traffic continue to increase after a return to normalcy? Will people be too scared to fly again? People tend to have a very short memory. Now, I’m not an expert in cognitive psychology, but people cannot see the virus. They cannot see buildings crumbling and a crater where one of the world’s tallest buildings used to be. The lack of visceral images renders the virus’s emotional impact less then it might have been otherwise. This leads to a normalcy bias of people minimizing the potential threat to their health and a resumption of pre-Covid behavior. Because of Ultra Low-Cost Carriers (ULCC), like Spirit, there has been continued passenger volume growth over the past decade. While economic downturns tend to decrease total Air demand, ULCCs tend not to be as adversely affected because of their inherent low-cost nature. It does dampen growth by reducing their non-ticket revenue which has become a driver of growth over the past few years. Over the past thirteen years, non-ticket revenue has grown tenfold and represents huge potential for the company. While the growth of this part of the company may stall, it will continue after the crisis and be a principal driver in Spirit’s growth.

The long term prospects of Spirit look bright. Firstly, the company has not been bogged down by the production problems at Boeing, by flying a completely Airbus fleet. The company “operat[es] a single-fleet type of Airbus A320-family aircraft that is one of the youngest and most fuel-efficient in the United States.” This flexibility allows crews to be completely interchangeable and is ruthlessly efficient. Additionally, the company can offer products significantly below the profitable price of other carriers. The largest foreseeable risk is when larger airlines begin offering ULCC rates for a set number of seats in their planes at a loss to take back market share. Such action may adversely affect Spirit’s ability to return outsized gains to its shareholders.

Philip Fischer is regarded as an investing legend and wrote “Common Stocks and Uncommon Profits”. In it, he delineated fourteen points which a company must possess if they will return significant value to shareholders over many years. The points can largely be summarized into four categories: Potential for Sales Growth, Margin growth, Management’s ability, and Labor relations.

The first question that must be asked is, what is Spirit’s potential for Sales growth. According to Statistica the total operating revenue of domestic airlines was $240 billion as of 2018.

Spirit Airlines sales were only $3.4 billion in 2019 and with a potential market of $240 billion, there is significant room for sales growth over the next decade.

The second point to observe is the future of the company’s margin. The current net margin of the company is ~8%. Such a low margin is not enticing, but Walmart and Costco succeed off of low margins with economies of scale and large volumes. As a ULCC Spirit will have low margins initially but will grow as scale is reached and additional passengers serve as pure profit. The ideal future for Spirit would be the American equivalent of Ryanair. Ryanair is a mature European ULCC. Ryanair initially had low net margins but grew them over time as scale was reached. Currently, their net margin is ~ 12% which is 50% higher than Spirit’s current net margin.

Ryanair net margin over time

From both a sales and margin perspective Spirit’s future looks bright. The next two points of discussion are labor and management. Most of Spirit’s workforce is unionized. Additionally, labor accounts for ~30% of operating costs and is extremely important to the Airline business. Adverse labor relations would crimp growth and ruin a potentially great company. However, given the preeminent position labor has in the company’s annual report, it should be safe to assume decent working conditions. Given the company’s low-cost structure pay is below the market average and may not attract the highest quality employees. My personal experience has always been positive when flying on Spirit and always had a positive experience with the employees.

With regards to management the CEO, Ted Christie III, has been with Spirit since 2012. Historically, companies that have promoted insiders to the helm have outperformed their peers that brought in outsiders. Also, the efficiency that Spirit operates with should testify to management’s capabilities.

The market has severely mispriced a growth company at bare bottom prices. Buying Spirit at its current price represents a great investment over the next decade. The company is efficiently managing its resources and has ample opportunity to increase its sales and profitability. The current market is pricing this wonderful company at criminally cheap levels.